SMM January 23: Macro factors, on November 15, with approval from the State Council, the Ministry of Commerce, in conjunction with the Ministry of Industry and Information Technology, the General Administration of Customs, and the State Cryptography Administration, issued Announcement No. 51 of 2024, releasing the "Export Control List of Dual-Use Items of the People's Republic of China." This list, effective from December 1, 2024, includes items related to antimony, germanium, gallium, magnesium-based biomaterials, among others.

In early December, the Ministry of Commerce announced that, in accordance with the relevant provisions of the "Export Control Law of the People's Republic of China" and other laws and regulations, to safeguard national security and interests and fulfill international obligations such as non-proliferation, it decided to strengthen export controls on related dual-use items to the US. The announcement specifies the following: 1. Prohibition of exports of dual-use items to US military users or for military purposes. 2. In principle, no licenses will be granted for the export of dual-use items related to gallium, germanium, antimony, and superhard materials to the US; stricter end-user and end-use reviews will be implemented for the export of dual-use graphite items to the US. Any organization or individual in any country or region that violates the above provisions by transferring or providing related dual-use items originating from the People's Republic of China to US organizations or individuals will be held legally accountable. This announcement took effect upon its release.

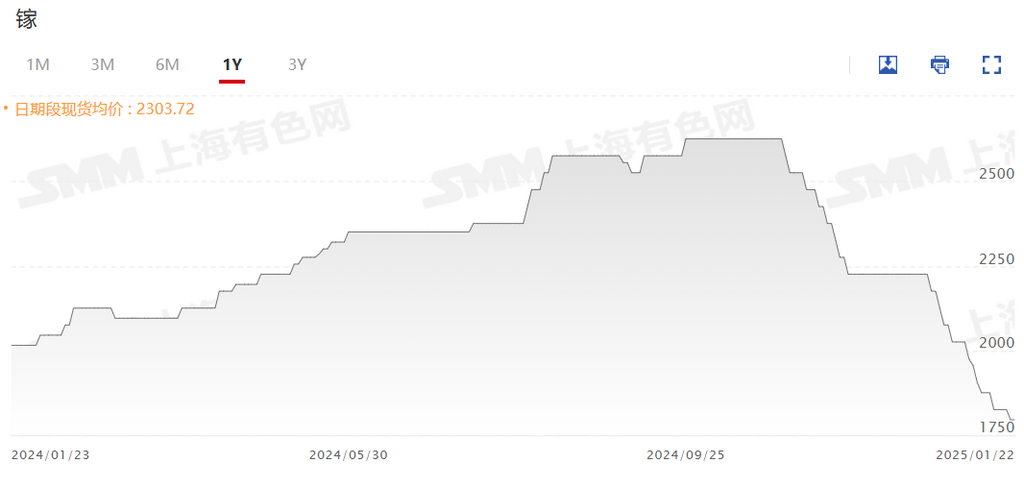

According to customs data, gallium exports in 2023 were approximately 45 mt, while customs data for January-November 2024 indicates gallium exports of around 54 mt. It is expected that the full-year customs data for 2024 will show significant growth compared to 2023. However, the policy announcements in November-December indicate that China's export control measures for metals such as gallium and germanium will remain stringent, or even become stricter. This suggests a potential decline in the overall export volume of gallium and germanium in the future (2025).

Fundamentally, from the supply side, in Q4, with the commissioning of gallium production lines by manufacturers such as Huajin, domestic gallium production continued to show a gradual upward trend. Given that the overall industry gross profit margin for gallium remains relatively high (estimated at around 40%), there is potential for further production growth in 2025 as output from manufacturers such as Pioneer Chongqing and Xinfa Fangyuan enters the market. For the overall production in 2024, the domestic gallium market's annual production is estimated to reach 770 mt, representing a slight increase compared to 2023.

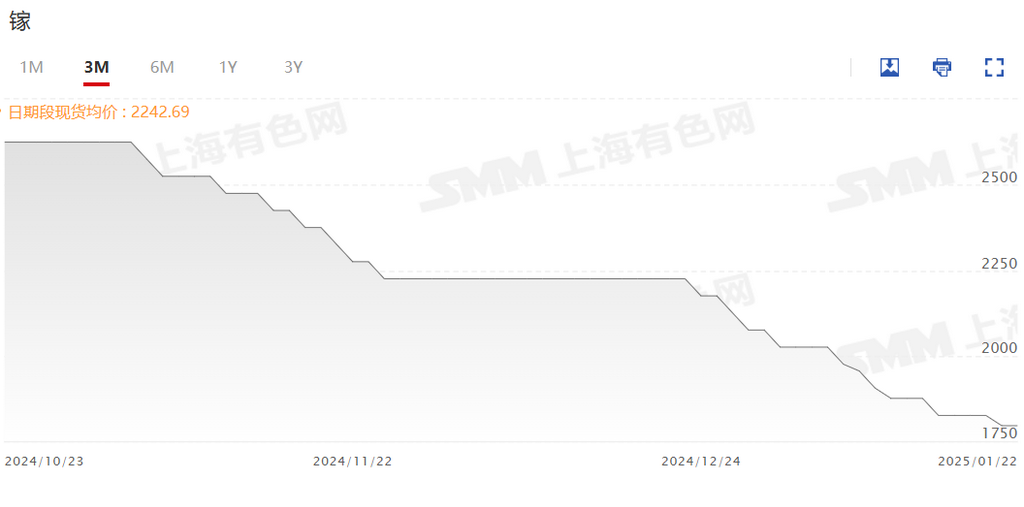

Demand side, in Q4, domestic demand slightly declined compared to Q3, mainly due to reduced gallium usage in the magnetic materials industry and decreased gallium consumption caused by lower PV production. Gallium consumption in the semiconductor sector remained relatively stable. For 2024 overall, the magnetic materials industry is estimated to consume around 145 mt of gallium, the PV industry approximately 80 mt, and the semiconductor sector about 330 mt. Including other industries, the actual gallium consumption in 2024 is estimated at around 630 mt, while the apparent consumption is estimated at 720 mt. This indicates that the gallium industry is currently in an inventory buildup phase, which has led to a weaker downward trend in gallium prices in Q4.

Market trend forecasts suggest that domestic gallium prices have shown an upward trend within a year after export controls were implemented, reflecting a certain degree of healthy self-circulation development in the domestic gallium industry. The price decline in Q4 was mainly influenced by reduced gallium consumption in the magnetic materials and PV industries, which is a short-term factor. The long-term impact remains unclear for now. However, the growth outlook for the magnetic materials industry remains optimistic. For instance, the annual compound growth rate of China's NEV demand for NdFeB permanent magnets is expected to reach 41%, with NdFeB permanent magnet production in China growing by 8-10% annually, and demand for NdFeB permanent magnets in China's variable frequency air conditioners increasing by 10-15% annually. Therefore, as long as there is no complete substitution of gallium in the magnetic materials industry, demand for gallium metal is expected to remain relatively stable. The same applies to the PV industry.

Looking ahead to 2025, after a year of supply and demand adjustments, gallium prices are expected to operate within a short-term range of 1,900-2,300 yuan/kg.

Issues Worth Noting

1. The greatest uncertainty still lies in changes in exports (application time for export qualifications, approval conditions, and other unknown factors), as well as the development speed of the semiconductor industry, which could impact both domestic and export prices.

2. The future development trends of the domestic semiconductor optoelectronics industry, including chip R&D, lithography machine manufacturing, and other currently popular sectors.

3. Whether the traditional stockpiling peak season for the semiconductor and magnetic materials industries will arrive as expected before and after the Chinese New Year holiday.